The term ‘behavioural science’ has been used loosely to cover many things across many industries over the last few years, so much so that the term has started to get a reputation as a buzzword.

Yet, behavioural science is so much more than a fancy buzzword.

While academia and government departments often lead the way in testing new approaches, private enterprises are increasingly getting involved in testing different psychological principles to drive customer behaviour.

With vast amounts of data at their disposal, it’s no surprise that tech companies, in particular, are leveraging behavioural science. However, there have been several examples of these companies using behavioural science to improve their bottom line at the expense of consumer freedom.

In 2017, a New York Times article exposed how Uber was leveraging techniques like loss aversion and goal-setting to keep drivers on the road for longer.

They even experimented with female vs male personas to see which is more effective at getting drivers on the road during a surge in customer demand. Many hotel aggregator websites have also found themselves in trouble for displaying nudges with manipulated data. For example, ‘This hotel has been booked 7 times in the past 24 hours’, even though it may not have been booked throughout the desired dates the user searches for.

Messages like these create a sense of scarcity and the user feels pressure to book instantly to ensure that they get the hotel room they want. Despite some evidence that consumers are wising up to ‘tricks’ like this, the question remains of how ethical it is to develop these nudges in the first place.

Earlier this year the Competition and Markets Authority (CMA) announced that it was taking enforcement action against sites such as Expedia and Booking.com to protect consumers from tactics that might be breaching consumer protection laws.

In the financial sector, we’ve yet to see behavioural science become fully embedded in mainstream financial products and journeys. Here at tomato pay (formerly Fractal), where our focus is on small business banking, we acknowledge that behavioural science techniques could easily be used to manipulate small and medium enterprises (SMEs) to mismanage their finances and take up unnecessary financial products.

We believe that win-win scenarios benefit both SMEs and financial innovators. SMEs should only be offered financial products they can afford and that further the long-term goal of business growth, not just survival. In return, financial innovators gain a larger, increasingly loyal SME customer base.

How can we ensure we prioritise building good money management habits over selling unnecessary financial products?

We’ve begun to develop our own ‘Ethics Pledge’.

The ambition is to have all of our partners sign this pledge before implementing our APIs. Some of these are specific to the SME financial journey, while others build on a libertarian, paternalistic approach, popular when discussing ethical issues around behavioural science interventions (Thaler, R. H., & Sunstein, C. R. (2003). Libertarian paternalism. American economic review, 93(2), 175-17).

Some of our initial ideas to include in the pledge:

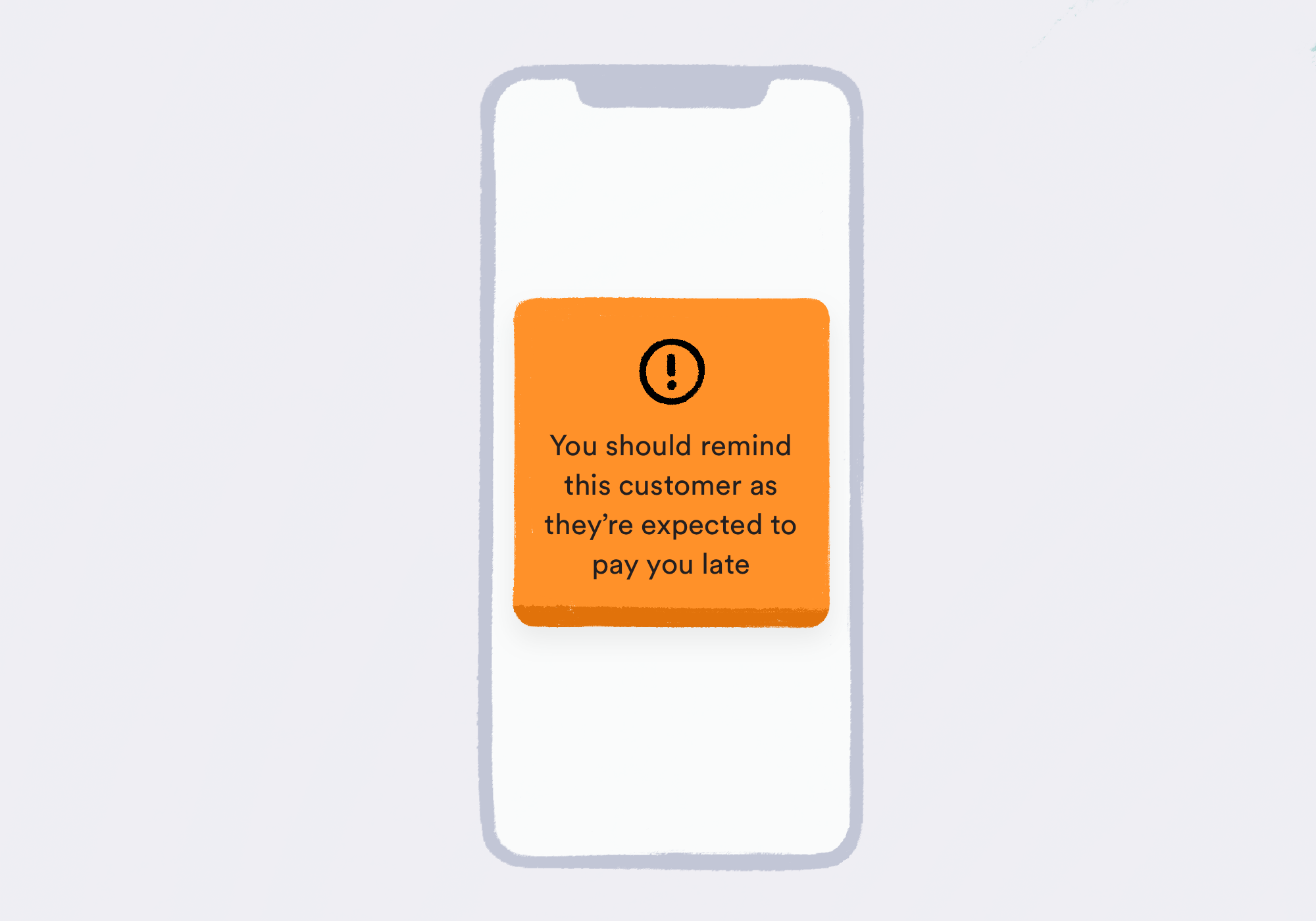

- Give a ‘soft’ nudge before a ‘hard’ nudge. We define any nudge that pushes a financial product as a ‘hard’ nudge. If, for example, our cash flow forecasting API shows a cash flow deficit coming up for an SME due to a late payment, then we should nudge them to chase the payment and get it in on time before nudging them to extend their overdraft facility to cover the deficit.

- Maintain freedom of choice. Partners should avoid making users feel that taking a financial product is the only option to address a scenario. They should also provide clear opt-out options during the product application process.

- Be transparent. Make it easy for users to understand how and why the platform uses behavioural science techniques, and also make it easy to opt-out of these features. Research shows that increasing the transparency of nudges does not decrease their impact. (Bruns, H., Kantorowicz-Reznichenko, E., Klement, K., Jonsson, M. L., & Rahali, B. (2018). Can nudges be transparent and yet effective?. Journal of Economic Psychology, 65, 41-59).

- Be welfare promoting. We believe that helping SMEs to fail less often, and grow faster, is best for everyone in the long run, so to consider their interests over short-term sales targets.

- Only use quality data to drive our insights. We actively discourage data manipulation, in particular when financial products are being promoted.

- Where possible, partners should measure the long term impact of using Fractal products on SME longevity, profitability and employment rates.

An important distinction we’ve made is to have a pledge as opposed to a policy.

Any behavioural economists out there will instantly recognise this as a ‘pre-commitment device’, a useful tool when trying to get people to stick to long-term goals and help them avoid any short-term temptation they may come up against. Pre-commitment pledges have been used to address several behavioural challenges, including reducing the number of people who do not show up for their GP appointment. The method used - having the patient write the date of their next appointment on a card as opposed to a receptionist.

While we can’t force adherence to the pledge, it’s a signal from both the tomato pay team and our partners that we are all committed to the ethical use of data and behavioural science.

As we look to scale and automate our use of behavioural science in our product, we believe a strong ethical approach is necessary. We’re beginning with a self-regulatory approach, of which our ethics pledge is the first step.

Now we want to open the floor to your input. Have you got any ideas of how we can ensure we treat our SME customers with respect and maximise their chances of succeeding?

Feel free to reach out to us on Twitter or LinkedIn with your ideas.